| • | have a potential positive credit ratings impact on the Company, as Moody’s Investor Services has publicly identified removing Genworth Life and Annuity Insurance Company from bankruptcy or insolvency and similar events of default under the Indenture as one of several factors that could lead to a ratings upgrade. |

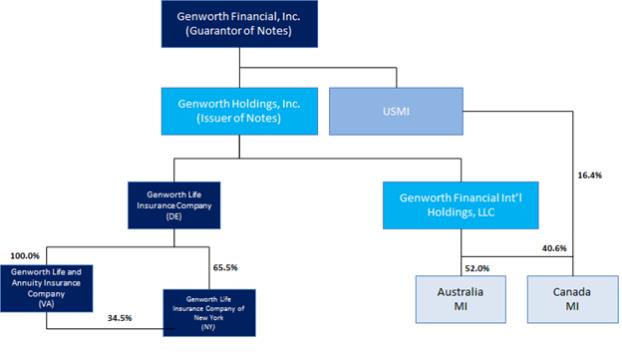

Simplified Organizational Chart

Proposed Amendments

If the Proposed Amendments are adopted, Section 6.01 of the Indenture would be amended with respect to each series of Notes by amending and restating the final paragraph of Section 6.01(h) to read as follows (with the proposed change underlined in bold):

For the avoidance of doubt, none of the bankruptcy, insolvency or other events described in Sections 6.01(f) and 6.01(g), if

they occur with respect to Genworth Life Insurance Company, Genworth Life and Annuity Insurance Company, and/or Genworth Life Insurance Company

of New York or any respective property thereof (including for the avoidance of doubt any subsidiary thereof), shall constitute an Event of Default.

The reference to Brookfield Life and Annuity Insurance Company would be deleted because it has been merged with and into Genworth Life Insurance Company.

Section 10.02 of the Indenture provides for the amendment of any provision of the Indenture related to a series of Notes (except certain provisions not relevant to the Consent Solicitation) by execution of a supplemental indenture upon the consent of Holders of at a majority in aggregate principal amount of the outstanding Notes of each series (each series voting as a separate class) affected by such supplemental indenture.

In respect of a series of Notes, upon the execution of the New Supplemental Indenture and the Proposed Amendments affecting such series of Notes becoming operative and upon the satisfaction of the conditions set forth in this Statement, including the receipt of the Requisite Consents with respect to such series of Notes, all Holders of

5