As filed with the Securities and Exchange Commission on May 24, 2004

Registration No. 333-115018

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 3

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Genworth Financial, Inc.

(Exact Name of Registrant as Specified in its Charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) |

6311 (Primary Standard Industrial Classification Code Number) |

33-1073076 (I.R.S. Employer Identification Number) |

||

6620 West Broad Street Richmond, Virginia 23230 (804) 281-6000 (Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant's Principal Executive Offices) |

||||

Leon E. Roday, Esq. Senior Vice President, General Counsel and Secretary Genworth Financial, Inc. 6620 West Broad Street Richmond, Virginia 23230 (804) 281-6000 (Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service) |

Copies to:

| David S. Lefkowitz, Esq. Corey R. Chivers, Esq. Weil, Gotshal & Manges LLP 767 Fifth Avenue New York, New York 10153 (212) 310-8000 |

Alexander M. Dye, Esq. LeBoeuf, Lamb, Greene & MacRae, L.L.P. 125 West 55th Street New York, New York 10019 (212) 424-8000 |

Richard J. Sandler, Esq. Davis Polk & Wardwell 450 Lexington Avenue New York, New York 10017 (212) 450-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. / /

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. / /

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. / /

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. / /

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. / /

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PROSPECTUS (Subject to Completion)

Issued May 24, 2004

2,000,000 Shares

% Series A Cumulative Preferred Stock

(Liquidation Preference $50 Per Share)

GE Financial Assurance Holdings, Inc., the selling stockholder and an indirect subsidiary of General Electric Company, or GE, is offering all the 2,000,000 shares of Series A Preferred Stock to be sold in this offering. Shares of Series A Preferred Stock will not be obligations of, and will not be guaranteed by, GE, the selling stockholder or our other affiliates. The Series A Preferred Stock will be mandatorily redeemable on , 2011 at $50 per share plus accumulated dividends. Dividends will be cumulative from the date of issuance and are payable quarterly, starting , 2004.

Concurrently with this offering, the selling stockholder is offering, by means of a separate prospectus, 145.0 million shares of our Class A Common Stock. Concurrently with this offering, the selling stockholder also is offering, by means of a separate prospectus, $600 million of our % Equity Units. Each Equity Unit will have a stated amount of $25 and will initially consist of a contract to purchase shares of our Class A Common Stock and an interest in a % senior note due 2009 issued by us. This offering of Series A Preferred Stock is contingent upon the completion of the offerings of our Class A Common Stock and Equity Units.

We will not receive any proceeds from the sale by the selling stockholder of Series A Preferred Stock in this offering or the Class A Common Stock or Equity Units in the concurrent offerings.

Investing in our Series A Preferred Stock involves risks. See "Risk Factors" beginning on page 15.

PRICE $50 A SHARE

| |

Per Share |

Total |

||

|---|---|---|---|---|

| Price to public | $ | $ | ||

| Underwriting discounts and commissions | $ | $ | ||

| Proceeds to seller | $ | $ |

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the Series A Preferred Stock to purchasers on , 2004.

Morgan Stanley |

Goldman, Sachs & Co. |

, 2004

| |

Page |

|

|---|---|---|

| Prospectus Summary | 1 | |

| Risk Factors | 15 | |

| Forward-Looking Statements | 45 | |

| Use of Proceeds | 46 | |

| Dividend Policy | 46 | |

| Capitalization | 47 | |

| Ratio of Earnings to Fixed Charges | 51 | |

| Selected Historical and Pro Forma Financial Information | 52 | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | 68 | |

| Corporate Reorganization | 131 | |

| Business | 134 | |

| Regulation | 214 | |

| Management | 225 | |

| Arrangements Between GE and Our Company | 248 | |

| Ownership of Common Stock | 276 | |

| Description of Series A Preferred Stock | 279 | |

| Description of Capital Stock | 286 | |

| Description of Equity Units | 297 | |

| Description of Certain Indebtedness | 302 | |

| Shares Eligible for Future Sale | 305 | |

| Certain United States Federal Income Tax Consequences | 307 | |

| Underwriters | 312 | |

| Legal Matters | 315 | |

| Experts | 315 | |

| Additional Information | 315 | |

| Index to Financial Statements | F-1 | |

| Glossary of Selected Insurance Terms | G-1 |

i

This summary highlights information contained elsewhere in this prospectus and may not contain all of the information that may be important to you. You should read this entire prospectus carefully, including the information set forth in "Risk Factors," before making an investment decision.

We are a leading insurance company in the U.S., with an expanding international presence, serving the life and lifestyle protection, retirement income, investment and mortgage insurance needs of more than 15 million customers. We have leadership positions in key products that we expect will benefit from a number of significant demographic, governmental and market trends. We distribute our products and services through an extensive and diversified distribution network that includes financial intermediaries, independent producers and dedicated sales specialists. We conduct operations in 20 countries and have approximately 5,850 employees.

We have the following three operating segments:

1

We also have a Corporate and Other segment, which consists primarily of net realized investment gains (losses), most of our interest and other financing expenses, unallocated corporate income and expenses, and the results of several small, non-core businesses that are managed outside our operating segments. For the year ended December 31, 2003 and the three months ended March 31, 2004, our Corporate and Other segment had a pro forma segment net loss of $8 million and pro forma segment net earnings of $8 million, respectively.

We had $12.3 billion of total stockholder's interest and $100.2 billion of total assets as of March 31, 2004, on a pro forma basis. For the year ended December 31, 2003 and the three months ended March 31, 2004, on a pro forma basis, our revenues were $9.8 billion and $2.6 billion, respectively, and our net earnings from continuing operations were $935 million and $266 million, respectively. Upon the completion of this offering, we expect our principal life insurance companies to have financial strength ratings of "AA-" (Very Strong) from S&P, "Aa3" (Excellent) from Moody's, "A+" (Superior) from A.M. Best and "AA-" (Very Strong) from Fitch, and we expect our rated mortgage insurance companies to have financial strength ratings of "AA" (Very Strong) from S&P, "Aa2" (Excellent) from Moody's and "AA" (Very Strong) from Fitch. The "AA" and "AA-" ratings are the third- and fourth-highest of S&P's 21 ratings categories, respectively. The "Aa2" and "Aa3" ratings are the third- and fourth-highest of Moody's 21 ratings categories, respectively. The "A+" rating is the second-highest of A.M. Best's 15 ratings categories. The "AA" and "AA-" ratings are the third- and fourth-highest of Fitch's 24 ratings categories, respectively.

Market Environment and Opportunities

We believe we are well positioned to benefit from a number of significant demographic, governmental and market trends, including the following:

Competitive Strengths

We believe the following competitive strengths will enable us to capitalize on opportunities in our targeted markets:

2

relationships. We refer to our approach to product diversity as "smart" breadth because we are selective in the products we offer and strive to maintain appropriate return and risk thresholds when we expand the scope of our product offerings.

Growth Strategies

Our objective is to increase operating earnings and enhance returns on equity. We intend to pursue this objective by focusing on the following strategies:

Retirement income, where we believe growth will be driven by a variety of favorable demographic trends and the approximately $4.4 trillion of invested financial assets in the U.S. that are held by people within 10 years of retirement. Our products are designed to enable the growing retired population to convert their invested assets into reliable retirement income.

Protection, particularly long-term care insurance, where we believe growth will be driven by the increasing protection needs of the expanding aging population and a shifting of the burden for funding these needs to individuals from governments and employers. For example, it is

3

estimated that approximately 70% of individuals in the U.S. aged 65 and older will require long-term care at some time in their lives, but in 2001, only 7% of individuals in the U.S. aged 55 and older had long-term care insurance.

International mortgage insurance, where we continue to see attractive growth opportunities with the expansion of homeownership and low-down-payment loans. The net premiums written in our international mortgage insurance business have increased by a compound annual growth rate of 46% for the three years ended December 31, 2003.

Product and service innovations, as illustrated by new product introductions, such as the introduction in 2002 of our GE Retirement Answer®, our introduction of innovative private mortgage insurance products in the European market, and our service innovations, which include programs such as our policyholder wellness initiatives in our long-term care insurance business and our AU Central® Internet platform in our mortgage insurance business.

Collaborative approach to key distributors, which includes a joint business improvement program (originally developed by GE), called "At the Customer, For the Customer," or ACFC, and our platinum customer service desks, which have benefited our distributors and helped strengthen our relationships with them.

Technology initiatives, such as our GENIUS® underwriting system, which makes it easier for distributors to do business with us, improves our term life and long-term care insurance underwriting speed and accuracy, and lowers our operating costs.

Rigorous product pricing and return discipline. We intend to maintain strict product pricing disciplines that are designed to achieve our target returns on capital. Over the past two years, we introduced restructured pricing on newly issued policies in each of our operating segments and exited products that were not achieving our target returns. We expect our returns on capital to improve as the benefits of these actions emerge and as we continue our focus on maintaining target returns.

Capital efficiency enhancements. We continually seek opportunities to use our capital more efficiently to support our business, while maintaining our ratings and strong capital position. For example, in 2003, we took actions to reduce the statutory capital required to support most of our new term and universal life insurance policies and to reduce excess capital at our mortgage insurance subsidiaries by operating at an "AA/Aa2" rating level.

Investment income enhancements. As part of GE, the yield on our investment portfolio has been affected by the practice in recent years of realizing investment gains through the sale of appreciated securities and other assets during a period of historically low interest rates. This strategy was pursued to offset impairments and losses in our investment portfolio, fund consolidations and restructurings in our business and provide current income. As we transition to being an independent public company, our investment strategy will be to optimize investment income without relying on realized investment gains. We will seek to improve our investment yield by continuously evaluating our asset class mix and pursuing additional investment classes.

Ongoing operating cost reductions and efficiencies. We will continually focus on reducing our cost base while maintaining strong service levels for our customers. We expect to accomplish

4

this in each of our operating units through a wide range of cost management disciplines, including consolidating operations, using low-cost operating locations, reducing supplier costs, leveraging Six Sigma and other process improvement efforts, forming dedicated teams to identify opportunities for cost reductions and investing in new technology, particularly for web-based, digital end-to-end processes.

Formation of Genworth Financial, Inc.

We were incorporated in Delaware on October 23, 2003 in preparation for our corporate reorganization and this offering.

Prior to the completion of this offering and the concurrent offerings, we will acquire substantially all of the assets and liabilities of GE Financial Assurance Holdings, Inc., or GEFAHI. GEFAHI is an indirect subsidiary of GE and a holding company for a group of companies that provide life insurance, long-term care insurance, group life and health insurance, annuities and other investment products and U.S. mortgage insurance. We also will acquire certain other insurance businesses currently owned by other GE subsidiaries but managed by members of the Genworth management team. These businesses include international mortgage insurance, European payment protection insurance, a Bermuda reinsurer and mortgage contract underwriting.

In consideration for the assets that we will acquire and the liabilities that we will assume in connection with our corporate reorganization, we will issue to GEFAHI the following securities:

5

The liabilities we will assume from GEFAHI include ¥60 billion aggregate principal amount of 1.6% notes due 2011 issued by GEFAHI, ¥3 billion of which GEFAHI currently owns and will transfer to us. We refer to these notes in this prospectus as the Yen Notes. We have entered into arrangements to swap our obligations under these notes to a U.S. dollar obligation with a principal amount of $491 million and bearing interest at a rate of 4.84% per annum.

Prior to the completion of this offering and the concurrent offerings, GEFAHI will own 100% of our outstanding common stock, which will consist solely of Class B Common Stock. Shares of Class B Common Stock convert automatically into shares of Class A Common Stock when they are held by any person other than GE or an affiliate of GE or when GE no longer beneficially owns at least 10% of our outstanding common stock. As a result, all the shares of common stock offered in the concurrent offering consist of Class A Common Stock. Upon the completion of this offering and the concurrent offerings, GE will beneficially own approximately 70% of our outstanding common stock, assuming the underwriters' over-allotment option in the concurrent offering of Class A Common Stock is not exercised, and 66%, if it is exercised in full. GE has informed us that, after completion of this offering, it intends, subject to market conditions, to divest its remaining interest in us as soon as practicable. GE has also informed us that, in any event, it expects to reduce its interest to below 50% within two years of the completion of this offering. GE currently expects to reduce its interest through one or more additional public offerings of our common stock, but it is not obligated to divest our shares in this or any other manner.

Prior to the completion of this offering, we will enter into a number of arrangements with GE governing our separation from GE and a variety of transition and other matters, including our relationship with GE while GE remains a significant stockholder in our company. These arrangements include several significant reinsurance transactions with Union Fidelity Life Insurance Company, or UFLIC, an indirect subsidiary of GE. As part of these transactions, we will cede to UFLIC, effective as of January 1, 2004, all of our in-force structured settlement contracts, substantially all of our in-force variable annuity contracts, and a block of long-term care insurance policies that we reinsured in 2000 from The Travelers Insurance Company, a subsidiary of Citigroup, Inc., which we refer to in this prospectus as Travelers. In the aggregate, these blocks of business do not meet our target return thresholds, and although we remain liable under these contracts and policies as the ceding insurer, the reinsurance transactions will have the effect of transferring the financial results of the reinsured blocks to UFLIC. We are continuing new sales of structured settlement, variable annuity and long-term care insurance products, and we expect to achieve our targeted returns on these new sales. In addition, we will continue to service these blocks of business, which will preserve our operating scale and enable us to service and grow our new sales of these products. See "Arrangements Between GE and Our Company."

6

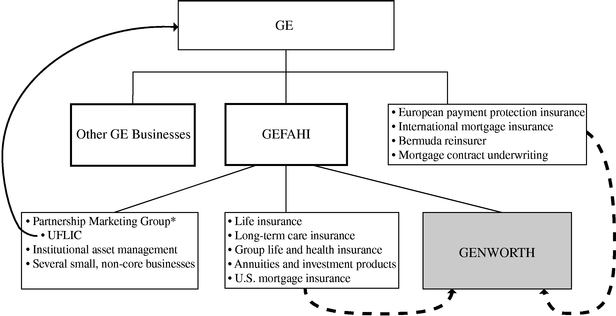

The diagram below shows the relationships among GE, GEFAHI and Genworth prior to the completion of our corporate reorganization. The dotted lines indicate the businesses that will be transferred to Genworth in connection with our corporate reorganization.

* The Partnership Marketing Group offers life and health insurance, auto club memberships and other financial products and services directly to consumers through affinity marketing arrangements with a variety of organizations. The Partnership Marketing Group historically included UFLIC, a subsidiary that offered the life and health insurance for these arrangements.

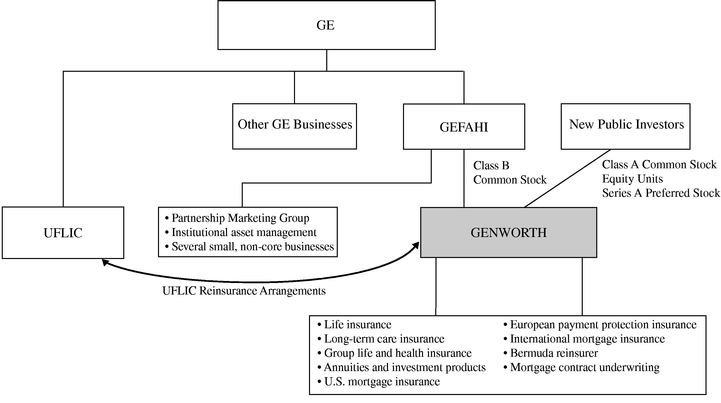

The diagram below shows the relationships among GE, GEFAHI and Genworth after the completion of our corporate reorganization and this offering.

In this prospectus, unless the context otherwise requires, "Genworth," "we," "us," and "our" refer to Genworth Financial, Inc. and its combined subsidiaries and include the operations of the businesses acquired from GEFAHI and other GE subsidiaries in connection with our corporate reorganization.

7

Risks Relating to Our Company

As part of your evaluation of our company, you should consider the risks associated with our business, our separation from GE and this offering. These risks include:

For a further discussion of these and other risks, see "Risk Factors."

Additional Information

Our corporate headquarters and principal executive offices are located at 6620 West Broad Street, Richmond, Virginia 23230. Our telephone number at that address is (804) 281-6000. We maintain a variety of websites to communicate with our distributors and customers and to provide information about various insurance and investment products to the general public. None of the information on our websites is part of this prospectus.

8

Issuer |

Genworth Financial, Inc. |

||

Series A Preferred Stock offered by the selling stockholder |

2,000,000 shares |

||

Preferred stock to be outstanding immediately after this offering |

2,000,000 shares |

||

Liquidation preference |

The liquidation preference for each share of the Series A Preferred Stock is the sum of $50 plus an amount equal to accrued and unpaid dividends on such share. See "Description of Series A Preferred Stock — Liquidation Rights." |

||

Mandatory redemption |

We are required to redeem the Series A Preferred Stock on , 2011 in whole at a price of $50 per share, plus unpaid dividends accrued to the date of redemption. There is no provision for early redemption of the Series A Preferred Stock. |

||

Dividends |

We will pay quarterly cash dividends on our Series A Preferred Stock, out of funds legally available for the payment thereof, at an annual rate equal to % of the sum of $50 per share plus the amount of the accumulated dividends, if any, accrued with respect to each share, commencing , 2004. Dividends for each full dividend period will be calculated by dividing the annual dividend rate by four. For any other dividend period including the initial dividend period, dividends will be calculated on the basis of a year of twelve 30-day months. See "Description of Series A Preferred Stock — Dividends." |

||

DRD protection |

If, prior to eighteen (18) months after the date of issuance of the shares of Series A Preferred Stock, one or more amendments to the Internal Revenue Code are enacted that reduce the "dividends-received deduction," or DRD, percentage (currently 70%), we will make certain payments in respect of the dividends on the Series A Preferred Stock and retroactive payments, except that no adjustments will be made with respect to any reduction of the dividends-received-percentage below 50%. See "Description of Series A Preferred Stock — Payments in Respect of Certain Legislation Affecting the DRD." |

||

Voting rights |

No voting rights, except as otherwise required by applicable law and the right to elect two additional directors during a default period, commencing when accumulated dividends have not been paid for six quarters, whether or not consecutive, or if we fail to discharge our mandatory redemption obligation. See "Description of Series A Preferred Stock — Voting Rights." |

||

Form and denominations |

The Series A Preferred Stock will be issued in the form of global securities held in book-entry form, in denominations of $50 of stated liquidation preference. Except as described in "Description of Series A Preferred Stock — Book-Entry System," Series A Preferred Stock in certificated form will not be issued in exchange for the global security. |

||

Ranking |

The Series A Preferred Stock will be effectively subordinated to all of our existing and future debt and other liabilities. As of March 31, 2004, on a pro forma basis, Genworth Financial, Inc. had outstanding $5,881 million of total liabilities at the holding company level, including $3,616 million of debt. See "Description of Certain Indebtedness." The Series A Preferred Stock also will be structurally subordinated to all debt and other liabilities of our subsidiaries (including liabilities to policyholders and contractholders), which means that creditors of our subsidiaries will be paid from their assets before holders of the Series A Preferred Stock would have any claims to those assets. As of March 31, 2004, on a pro forma basis, our subsidiaries had outstanding $82,057 million of total liabilities, including $1,573 million of debt (excluding, in each case, intercompany liabilities). See "Risk Factors—Risks Relating to Our Businesses—As a holding company, we depend on the ability of our subsidiaries to transfer funds to us to pay dividends and to meet our obligations" and "Description of Series A Preferred Stock." |

||

9

Use of proceeds |

We will not receive any proceeds from the sale by the selling stockholder of Series A Preferred Stock in this offering or of the Class A Common Stock or the Equity Units in the concurrent offerings. |

||

Listing |

We do not intend to apply for listing of the Series A Preferred Stock on any securities exchange or for quotation of the Series A Preferred Stock in any automated dealer quotation system. The underwriters have advised us that they currently intend to make a market in the Series A Preferred Stock. However, the underwriters are not obligated to do so, and any market-making with respect to the Series A Preferred Stock may be discontinued at any time without notice. |

||

Concurrent offerings |

Concurrently with this offering, the selling stockholder is publicly offering, by separate prospectuses: |

||

Class A Common Stock |

145.0 million shares of our Class A Common Stock, plus up to an additional 21.75 million shares that may be sold pursuant to an over-allotment option. |

||

Equity Units |

$600 million of our % Equity Units. |

||

Conditions |

The offerings of the Class A Common Stock and Equity Units are conditioned upon the completion of this offering. This offering is conditioned upon the completion of the offerings of the Class A Common Stock and the Equity Units. |

||

Unless otherwise indicated, all information in this prospectus:

10

The number of our stock options, restricted stock units and stock appreciation rights that will be issued in exchange for GE stock options, restricted stock units and stock appreciation rights will depend upon the initial public offering price of our Class A Common Stock in that concurrent offering and the weighted-average stock price of GE common stock for the trading day immediately prior to the date of this prospectus. Information in this prospectus assumes a price of $30.85 per share of GE common stock, which was the weighted-average stock price on April 27, 2004.

11

Summary Historical and Pro Forma Financial Information

The following table sets forth summary historical combined and pro forma financial information. You should read this information in conjunction with the information under "Selected Historical and Pro Forma Financial Information," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our combined financial statements and the related notes included elsewhere in this prospectus.

Prior to the completion of this offering, we will acquire substantially all of the assets and liabilities of GEFAHI. We also will acquire certain other insurance businesses currently owned by other GE subsidiaries but managed by members of the Genworth management team. These businesses include international mortgage insurance, European payment protection insurance, a Bermuda reinsurer and mortgage contract underwriting. In consideration for the assets that we will acquire and the liabilities that we will assume in connection with our corporate reorganization, we will issue to GEFAHI 489.5 million shares of our Class B Common Stock, $600 million of our Equity Units, $100 million of our Series A Preferred Stock, the $2.4 billion Short-term Intercompany Note and the $550 million Contingent Note.

We have prepared our combined financial statements as if Genworth had been in existence throughout all relevant periods. Our historical combined financial information and statements include all businesses that were owned by GEFAHI including those that will not be transferred to us, as well as the other insurance businesses that we will acquire from other GE subsidiaries, each in connection with our corporate reorganization.

The unaudited pro forma information set forth below reflects our historical combined financial information, as adjusted to give effect to the transactions described under "Selected Historical and Pro Forma Financial Information" as if each had occurred as of January 1, 2003, in the case of earnings information, and March 31, 2004, in the case of financial position information. The following transactions are reflected in the pro forma financial information:

The unaudited pro forma information below is based upon available information and assumptions that we believe are reasonable. The unaudited pro forma financial information is for illustrative and informational purposes only and is not intended to represent or be indicative of what our financial condition or results of operations would have been had the transactions described above occurred on the dates indicated. The unaudited pro forma information also should not be considered representative of our future financial condition or results of operations.

In addition to the pro forma adjustments to our historical combined financial statements, various other factors will have an effect on our financial condition and results of operations after the completion of this offering, including those discussed under "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations."

12

| |

Historical |

Pro forma |

|||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Three months ended March 31, |

Years ended December 31, |

Three months ended March 31, |

Year ended December 31, |

|||||||||||||||||||||||||||||||

| (Amounts in millions, except per share amounts) |

2004 |

2003 |

2003(1) |

2002 |

2001 |

2000(2) |

1999 |

2004 |

2003 |

2003 |

|||||||||||||||||||||||||

| Combined Statement of Earnings Information |

|||||||||||||||||||||||||||||||||||

| Revenues: | |||||||||||||||||||||||||||||||||||

| Premiums | $ | 1,722 | $ | 1,587 | $ | 6,703 | $ | 6,107 | $ | 6,012 | $ | 5,233 | $ | 4,534 | $ | 1,619 | $ | 1,478 | $ | 6,252 | |||||||||||||||

| Net investment income | 1,020 | 992 | 4,015 | 3,979 | 3,895 | 3,678 | 3,440 | 755 | 721 | 2,928 | |||||||||||||||||||||||||

| Net realized investment gains | 16 | 21 | 10 | 204 | 201 | 262 | 280 | 15 | 20 | 38 | |||||||||||||||||||||||||

| Policy fees and other income | 263 | 231 | 943 | 939 | 993 | 1,053 | 751 | 166 | 135 | 557 | |||||||||||||||||||||||||

| Total revenues | 3,021 | 2,831 | 11,671 | 11,229 | 11,101 | 10,226 | 9,005 | 2,555 | 2,354 | 9,775 | |||||||||||||||||||||||||

Benefits and expenses: |

|||||||||||||||||||||||||||||||||||

| Benefits and other changes in policy reserves | 1,348 | 1,253 | 5,232 | 4,640 | 4,474 | 3,586 | 3,286 | 1,086 | 996 | 4,191 | |||||||||||||||||||||||||

| Interest credited | 396 | 409 | 1,624 | 1,645 | 1,620 | 1,456 | 1,290 | 330 | 343 | 1,358 | |||||||||||||||||||||||||

| Underwriting, acquisition, and insurance expenses, net of deferrals |

508 | 488 | 1,942 | 1,808 | 1,823 | 1,813 | 1,626 | 414 | 404 | 1,614 | |||||||||||||||||||||||||

| Amortization of deferred acquisition costs and intangibles(3) |

345 | 300 | 1,351 | 1,221 | 1,237 | 1,394 | 1,136 | 286 | 251 | 1,144 | |||||||||||||||||||||||||

| Interest expense | 47 | 27 | 140 | 124 | 126 | 126 | 78 | 45 | 26 | 138 | |||||||||||||||||||||||||

| Total benefits and expenses | 2,644 | 2,477 | 10,289 | 9,438 | 9,280 | 8,375 | 7,416 | 2,161 | 2,020 | 8,445 | |||||||||||||||||||||||||

Earnings from continuing operations before income taxes |

377 |

354 |

1,382 |

1,791 |

1,821 |

1,851 |

1,589 |

394 |

334 |

1,330 |

|||||||||||||||||||||||||

| Provision for income taxes | 117 | 100 | 413 | 411 | 590 | 576 | 455 | 128 | 94 | 395 | |||||||||||||||||||||||||

| Net earnings from continuing operations | $ | 260 | $ | 254 | $ | 969 | $ | 1,380 | $ | 1,231 | $ | 1,275 | $ | 1,134 | $ | 266 | $ | 240 | $ | 935 | |||||||||||||||

Pro forma earnings from continuing operations per share: |

|||||||||||||||||||||||||||||||||||

| Basic | $ | 0.53 | $ | 0.52 | $ | 1.98 | $ | 0.54 | $ | 0.49 | $ | 1.91 | |||||||||||||||||||||||

| Diluted | $ | 0.53 | $ | 0.52 | $ | 1.98 | $ | 0.54 | $ | 0.49 | $ | 1.91 | |||||||||||||||||||||||

| Pro forma shares outstanding: | |||||||||||||||||||||||||||||||||||

| Basic | 489.5 | 489.5 | 489.5 | 489.5 | 489.5 | 489.5 | |||||||||||||||||||||||||||||

| Diluted | 490.0 | 490.0 | 490.0 | 490.0 | 490.0 | 490.0 | |||||||||||||||||||||||||||||

Selected Segment Information |

|||||||||||||||||||||||||||||||||||

| Total revenues: | |||||||||||||||||||||||||||||||||||

| Protection | $ | 1,566 | $ | 1,472 | $ | 6,153 | $ | 5,605 | $ | 5,443 | $ | 4,917 | $ | 1,489 | $ | 1,393 | $ | 5,839 | |||||||||||||||||

| Retirement Income and Investments | 976 | 958 | 3,781 | 3,756 | 3,721 | 3,137 | 725 | 689 | 2,707 | ||||||||||||||||||||||||||

| Mortgage Insurance | 263 | 227 | 982 | 946 | 965 | 895 | 263 | 227 | 982 | ||||||||||||||||||||||||||

| Affinity(4) | 139 | 137 | 566 | 588 | 687 | 817 | — | — | — | ||||||||||||||||||||||||||

| Corporate and Other | 77 | 37 | 189 | 334 | 285 | 460 | 78 | 45 | 247 | ||||||||||||||||||||||||||

| Total | $ | 3,021 | $ | 2,831 | $ | 11,671 | $ | 11,229 | $ | 11,101 | $ | 10,226 | $ | 2,555 | $ | 2,354 | $ | 9,775 | |||||||||||||||||

Net earnings (loss) from continuing operations: |

|||||||||||||||||||||||||||||||||||

| Protection | $ | 124 | $ | 131 | $ | 487 | $ | 554 | $ | 538 | $ | 492 | $ | 123 | $ | 124 | $ | 481 | |||||||||||||||||

| Retirement Income and Investments | 31 | 42 | 151 | 186 | 215 | 250 | 32 | 26 | 93 | ||||||||||||||||||||||||||

| Mortgage Insurance | 103 | 85 | 369 | 451 | 428 | 414 | 103 | 85 | 369 | ||||||||||||||||||||||||||

| Affinity(4) | (2 | ) | — | 16 | (3 | ) | 24 | (13 | ) | — | — | — | |||||||||||||||||||||||

| Corporate and Other | 4 | (4 | ) | (54 | ) | 192 | 26 | 132 | 8 | 5 | (8 | ) | |||||||||||||||||||||||

| Total | $ | 260 | $ | 254 | $ | 969 | $ | 1,380 | $ | 1,231 | $ | 1,275 | $ | 266 | $ | 240 | $ | 935 | |||||||||||||||||

13

| |

Historical |

Pro forma |

|||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

March 31, |

December 31, |

March 31, |

||||||||||||||||||||

| (Dollar amounts in millions) |

2004 |

2003(1) |

2002 |

2001 |

2000(2) |

1999 |

2004 |

||||||||||||||||

| Combined Statement of Financial Position Information |

|||||||||||||||||||||||

| Total investments | $ | 81,466 | $ | 78,693 | $ | 72,080 | $ | 62,977 | $ | 54,978 | $ | 48,341 | $ | 61,749 | |||||||||

| All other assets | 25,070 | 24,738 | 45,277 | 41,021 | 44,598 | 27,758 | 38,457 | ||||||||||||||||

| Total assets | $ | 106,536 | $ | 103,431 | $ | 117,357 | $ | 103,998 | $ | 99,576 | $ | 76,099 | $ | 100,206 | |||||||||

Policyholder liabilities |

$ |

67,346 |

$ |

66,545 |

$ |

63,195 |

$ |

55,900 |

$ |

48,291 |

$ |

45,042 |

$ |

66,841 |

|||||||||

| Non-recourse funding obligations(5) | 600 | 600 | — | — | — | — | 600 | ||||||||||||||||

| Short-term borrowings | 2,496 | 2,239 | 1,850 | 1,752 | 2,258 | 990 | 2,400 | ||||||||||||||||

| Long-term borrowings | 516 | 529 | 472 | 622 | 175 | 175 | 516 | ||||||||||||||||

| All other liabilities | 18,153 | 17,718 | 35,088 | 31,559 | 35,865 | 18,646 | 17,581 | ||||||||||||||||

| Total liabilities | $ | 89,111 | $ | 87,631 | $ | 100,605 | $ | 89,833 | $ | 86,589 | $ | 64,853 | $ | 87,938 | |||||||||

| Accumulated nonowner changes in stockholder's interest | $ | 2,976 | $ | 1,672 | $ | 835 | $ | (664 | ) | $ | (424 | ) | $ | (862 | ) | $ | 1,987 | ||||||

| Total stockholder's interest | 17,425 | 15,800 | 16,752 | 14,165 | 12,987 | 11,246 | 12,268 | ||||||||||||||||

U.S. Statutory Information |

|||||||||||||||||||||||

Statutory capital and surplus(6) |

7,129 |

7,021 |

7,207 |

7,940 |

7,119 |

6,140 |

|||||||||||||||||

| Asset valuation reserve | 453 | 413 | 390 | 477 | 497 | 500 | |||||||||||||||||

14

You should carefully consider the following risks before investing in our Series A Preferred Stock. These risks could materially affect our business, results of operations or financial condition and cause the trading price of our Series A Preferred Stock to decline. You could lose part or all of your investment.

Risks Relating to Our Businesses

Interest rate fluctuations could adversely affect our business and profitability.

Our insurance and investment products are sensitive to interest rate fluctuations and expose us to the risk that falling interest rates will reduce our "spread," or the difference between the returns we earn on the investments that support our obligations under these products and the amounts that we must pay policyholders and contractholders. Because we may reduce the interest rates we credit on most of these products only at limited, pre-established intervals, and because some of them have guaranteed minimum crediting rates, declines in interest rates may adversely affect the profitability of those products. For example, interest rates declined to unusually low levels from 2001 to 2003. During this period, our net earnings from spread-based products, such as fixed and income annuities and guaranteed investment contracts, declined from $207 million for the year ended December 31, 2001 to $138 million for the year ended December 31, 2003.

During periods of increasing market interest rates, we must offer higher crediting rates on interest-sensitive products, such as universal life insurance and fixed annuities, and we must increase crediting rates on in-force products to keep these products competitive. In addition, increases in market interest rates may cause increased policy surrenders, withdrawals from life insurance policies and annuity contracts and requests for policy loans, as policyholders and contractholders seek to shift assets to products with perceived higher returns. Increases in crediting rates, as well as surrenders and withdrawals, could have an adverse effect on our financial condition and results of operations. An increase in policy surrenders and withdrawals also may require us to accelerate amortization of deferred acquisition costs or other intangibles or cause an impairment of goodwill, which would reduce our net earnings.

Our long-term care insurance products also expose us to the risk of interest rate fluctuations. The pricing and expected future profitability of these products are based in part on expected investment returns. Over time, long-term care insurance products generally produce positive cash flows as customers pay periodic premiums, which we invest as we receive them. Declining interest rates may reduce our ability to achieve our targeted investment margins and may adversely affect the profitability of our long-term care insurance products.

In our mortgage insurance business, rising interest rates generally reduce the volume of new mortgages, resulting in a decrease in the volume of new insurance written. Rising interest rates also can increase the monthly mortgage payments for insured homeowners with adjustable rate mortgages, or ARMs, which could have the effect of increasing default rates on ARM loans and thereby increasing our exposure on our mortgage insurance policies. This is particularly relevant in our non-U.S. mortgage insurance business, where ARMs are the predominant mortgage product. Declining interest rates increase the rate at which insured borrowers refinance their existing mortgages, thereby resulting in cancellations of the mortgage insurance covering the refinanced loans. Declining interest rates also generally are associated with home price appreciation, which may provide insured borrowers the option of canceling their mortgage insurance coverage earlier than we anticipated in pricing that coverage. These cancellations could have an adverse effect on our results from our mortgage insurance business.

Interest rate fluctuations also could have an adverse effect on the results of our investment portfolio. During periods of declining market interest rates, the interest we receive on variable interest rate investments decreases. In addition, during those periods, we are forced to reinvest the cash we receive as interest or return of principal on our investments in lower-yielding high-grade instruments or in lower-credit instruments to maintain comparable returns. Issuers of fixed-income securities also may decide to prepay their obligations in order to borrow at lower market rates, which exacerbates the risk

15

that we may have to invest the cash proceeds of these securities in lower-yielding or lower-credit instruments. Declining interest rates from 2001 to 2003 contributed to a decrease in our weighted average investment yield from 6.5% for the year ended December 31, 2001 to 5.2% for the year ended December 31, 2003. For additional information regarding our investment portfolio, see "Business—Investments." For additional information regarding the sensitivity of the fixed maturities in our investment portfolio to interest rate fluctuations, see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Quantitative and Qualitative Disclosures About Market Risk—Sensitivity analysis."

Downturns and volatility in equity markets could adversely affect our business and profitability.

Significant downturns and volatility in equity markets could have an adverse effect on our financial condition and results of operations in three principal ways. First, market downturns and volatility may cause potential new purchasers of our products to refrain from purchasing products, such as variable annuities and variable life insurance, that have returns linked to the performance of the equity markets and may cause current policyholders and contractholders to withdraw cash values from those products. The sharp declines in the equity markets during 2001 and 2002 have had adverse impacts on our sales of variable annuities and other products linked to equity markets. For example, our deposits for variable annuities decreased by 28% from $2,309 million for the year ended December 31, 2001 to $1,667 million for the year ended December 31, 2002.

Second, downturns and volatility in equity markets can have an adverse effect on the revenues and returns from our separate account and private asset management products and services. Because these products depend on fees related primarily to the value of assets under management, declines in the equity markets have reduced our revenues by reducing the value of the investment assets we manage. For example, the recent equity market downturn caused a reduction in the value of the separate account assets underlying our variable life insurance policies, variable annuities and assets under management. As a result, our policy fees and other income in our Retirement Income and Investments segment decreased by 7% from $243 million for the year ended December 31, 2002 to $225 million for the year ended December 31, 2003. In addition, some of our variable annuity products contain guaranteed minimum death benefits and guaranteed minimum income payments tied to the investment performance of the assets held within the variable annuity. A significant market decline could result in declines in account values which could increase our payments under the guaranteed minimum death benefits and certain income payments in connection with variable annuities, which could have an adverse effect on our financial condition and results of operations.

Third, we are exposed to equity risk on our holdings of common stock and other equities. An economic downturn, corporate malfeasance or a variety of other factors could cause declines in the value of our equity portfolio and cause our net earnings to decline. For additional information regarding the sensitivity of the equity securities in our investment portfolio to equity market fluctuations, see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Quantitative and Qualitative Disclosures About Market Risk—Sensitivity analysis."

Defaults in our fixed-income securities portfolio may reduce our earnings.

Issuers of the fixed-income securities that we own may default on principal and interest payments. As of each of March 31, 2004 and December 31, 2003 and 2002, 93% of our fixed maturities had ratings equivalent to investment-grade. Nevertheless, as a result of the economic downturn and recent corporate malfeasance, the number of companies defaulting on their debt obligations increased dramatically in 2001 and 2002. As of March 31, 2004 and December 31, 2003 and 2002, we had fixed maturities in or near default (where the issuer has missed payment of principal or interest or entered bankruptcy) with a fair value of $177 million, $190 million and $181 million, respectively. An economic downturn, further events of corporate malfeasance or a variety of other factors could cause declines in the value of our fixed maturities porfolio and cause our net earnings to decline.

16

We recognized gross capital gains of $27 million, $181 million, $473 million, $790 million and $814 million for the three months ended March 31, 2004 and 2003 and the years ended December 31, 2003, 2002 and 2001, respectively. We realized these capital gains in part to offset default-related losses during those periods. However, capital gains may not be available in the future, and if they are, we may elect not to recognize capital gains to offset losses.

A downgrade or a potential downgrade in our financial strength or credit ratings could result in a loss of business and adversely affect our financial condition and results of operations.

Financial strength ratings, which various ratings organizations publish as measures of an insurance company's ability to meet contractholder and policyholder obligations, are important to maintaining public confidence in our products, the ability to market our products and our competitive position. A downgrade in our financial strength ratings, or the announced potential for a downgrade, could have a significant adverse effect on our financial condition and results of operations in many ways, including:

In connection with our initial public offering and separation from GE, our principal life insurance companies were downgraded from financial strength ratings of "AA" (Very Strong) by S&P and "Aa2" (Excellent) by Moody's, to "AA-" (Very Strong) and "Aa3" (Excellent), respectively. In addition, as a result of our 2003 decision to reduce excess capital at our mortgage insurance subsidiaries, our mortgage insurance companies were downgraded from financial strength ratings of "AAA" (Extremely Strong) by S&P and Fitch and "Aaa" (Exceptional) by Moody's to "AA" (Very Strong) by S&P and Fitch and "Aa2" (Excellent) by Moody's. Although we do not believe that these downgrades have negatively affected our business overall in any material respect, we cannot assure you that they will not have an adverse effect over time or that our ratings will not be further downgraded in the future. The "AA" and "AA-" ratings are the third- and fourth-highest of S&P's 21 ratings categories, respectively. The "Aa2" and "Aa3" ratings are the third- and fourth-highest of Moody's 21 ratings categories, respectively. The "AA" rating is the third-highest of Fitch's 24 ratings categories.

The charters of the Federal National Mortgage Corporation, or Fannie Mae, and the Federal Home Loan Mortgage Corporation, or Freddie Mac, only permit them to buy high loan-to-value mortgages that are insured by a "qualified insurer," as determined by each of them. Their current rules effectively provide that they will accept mortgage insurance only from private mortgage insurers with financial strength ratings of at least "AA-" by S&P and "Aa3" by Moody's. If our mortgage insurance companies' financial strength ratings decrease below the thresholds established by Fannie Mae and Freddie Mac, we would not be able to insure mortgages purchased by Fannie Mae or Freddie Mac. Approximately 69% and 68% of the loans we insured in the U.S. during the three months ended March 31, 2004 and the year ended December 31, 2003, respectively, were sold to either Fannie Mae or Freddie Mac. An inability to insure mortgage loans sold to Fannie Mae or Freddie Mac, or their transfer of our existing policies to an alternative mortgage insurer, would have an adverse effect on our financial condition and results of operations.

In 2003, the U.S. Office of Federal Housing Enterprise Oversight announced a risk-based capital rule that treats credit enhancements issued by private mortgage insurers with financial strength ratings of "AAA" more favorably than those issued by "AA" rated insurers. Neither Fannie Mae nor Freddie Mac has adopted policies that distinguish between "AA" rated and "AAA" rated mortgage insurers.

17

However, if Fannie Mae or Freddie Mac adopts policies that treat "AAA" rated insurers more favorably than "AA" rated insurers, our competitive position may suffer.

Our mortgage insurance subsidiaries in Canada and Australia are also subject to local regulations that require them to maintain specified financial strength ratings to continue their operations.

In addition to the financial strength ratings of our insurance subsidiaries, ratings agencies also publish credit ratings for our company. The credit ratings have an impact on the interest rates we pay on the money we borrow. Therefore, a downgrade in our credit ratings could increase our cost of borrowing and have an adverse effect on our financial condition and results of operations.

The ratings of our insurance subsidiaries are not evaluations directed to the protection of investors in our common stock.

The ratings of our insurance subsidiaries described under "Business—Financial Strength Ratings" reflect each rating agency's current opinion of each subsidiary's financial strength, operating performance and ability to meet obligations to policyholders and contractholders. These factors are of concern to policyholders, contractholders, agents, sales intermediaries and lenders. Ratings are not evaluations directed to the protection of investors in our common stock. They are not ratings of our common stock and should not be relied upon when making a decision to buy, hold or sell our shares of common stock or any other security. In addition, the standards used by rating agencies in determining financial strength are different from capital requirements set by state insurance regulators. We may need to take actions in response to changing standards set by any of the ratings agencies, as well as statutory capital requirements, which could cause our business and operations to suffer.

If our reserves for future policy benefits and claims are inadequate, we may be required to increase our reserve liabilities, which could adversely affect our results of operations and financial condition.

We establish reserve liabilities to provide for future obligations under our insurance policies, annuities and other investment products, and mortgage insurance contract underwriting arrangements. Reserves do not represent an exact calculation of liability, but rather are estimates of expected net policy and contract benefits and claims payments over time. Our reserving assumptions and estimates require significant judgments and, therefore, are inherently uncertain. We cannot determine with precision the ultimate amounts that we will pay for actual benefit and claim payments, the timing of those payments, or whether the assets supporting our policy and contract liabilities will increase to the levels we estimate before payment of benefits or claims. We continually monitor our reserves. If we conclude that our reserves are insufficient to cover actual or expected policy and contract benefits and claims payments, we would be required to increase our reserves and incur income statement charges for the period in which we make the determination, which could adversely affect our results of operations and financial condition. For more information on how we set our reserves, see "Business—Reserves."

As a holding company, we depend on the ability of our subsidiaries to transfer funds to us to pay dividends and to meet our obligations.

We will act as a holding company for our insurance subsidiaries and will not have any significant operations of our own. Dividends from our subsidiaries and permitted payments to us under our tax sharing arrangements with our subsidiaries will be our principal sources of cash to pay stockholder dividends and to meet our obligations. These obligations will include our operating expenses, interest and principal on debt and contract adjustment payments on our Equity Units. These obligations also include amounts we will owe to GE under the tax matters agreement that we and GE will enter into prior to the completion of this offering. If the cash we receive from our subsidiaries pursuant to dividend payment and tax sharing arrangements is insufficient for us to fund any of these obligations, we may be required to raise cash through the incurrence of debt, the issuance of additional equity or the sale of assets.

18

The payment of dividends and other distributions to us by our insurance subsidiaries is regulated by insurance laws and regulations. In general, dividends in excess of prescribed limits are deemed "extraordinary" and require insurance regulatory approval. See "Regulation." During the years ended December 31, 2003, 2002 and 2001, we received dividends from our insurance subsidiaries of $1,472 million ($1,400 million of which were deemed "extraordinary"), $840 million ($375 million of which were deemed "extraordinary") and $410 million (none of which were deemed "extraordinary"), respectively. In addition, during the years ended December 31, 2003, 2002 and 2001, we received dividends from insurance subsidiaries related to discontinued operations of $495 million, $62 million and $0, respectively. Based on statutory results as of December 31, 2003, our subsidiaries could pay dividends of $1,121 million to us in 2004 without obtaining regulatory approval. However, as a result of the dividends we will pay in connection with our corporate reorganization, most of our insurance subsidiaries will not be able to pay us any additional dividends for the twelve months following this offering without prior regulatory approval. As part of our corporate reorganization, we will retain cash at the holding company level which we believe will be adequate to fund our dividend payments, debt service, obligations under the tax matters agreement and other obligations until our subsidiaries can resume paying dividends to us. In addition, the ability of our insurance subsidiaries to pay dividends to us, and our ability to pay dividends to our stockholders, are subject to various conditions imposed by the rating agencies for us to maintain our ratings.

Some of our investments are relatively illiquid.

Our investments in privately placed fixed maturities, mortgage loans, policy loans, limited partnership interests, real estate and restricted investments held by securitization entities are relatively illiquid. These asset classes represented approximately 30% of the carrying value of our total cash and invested assets as of March 31, 2004, on a pro forma basis. If we require significant amounts of cash on short notice in excess of our normal cash requirements, we may have difficulty selling these investments in a timely manner, be forced to sell them for less than we otherwise would have been able to realize, or both. For example, our floating rate funding agreements generally contain "put" provisions through which a contractholder may terminate the funding agreement for any reason after giving notice within the contract's specified notice period, which is generally 90 days but can be less than 30 days. As of March 31, 2004, the aggregate amount of our outstanding funding agreements with put option features was approximately $2.4 billion, and the aggregate amount of funding agreements with put option notice periods of 30 days or less was $450 million. If an unexpected number of contractholders exercise this right and we are unable to access other liquidity sources, we may have to liquidate assets quickly. Our inability to quickly dispose of illiquid investments could have an adverse effect on our financial condition and results of operations.

Intense competition could negatively affect our ability to maintain or increase our market share and profitability.

Our businesses are subject to intense competition. We believe the principal competitive factors in the sale of our products are product features, price, commission structure, marketing and distribution arrangements, brand, reputation, financial strength ratings and service.

Many other companies actively compete for sales in our protection and retirement income and investments markets, including other major insurers, banks, other financial institutions and specialty providers. The principal direct and indirect competitors for our mortgage insurance business include other private mortgage insurers, as well as federal and state governmental and quasi-governmental agencies in the U.S., including the Federal Housing Administration, or FHA, and to a lesser degree, the Veterans Administration, or VA, Fannie Mae and Freddie Mac, as well as local and state housing finance agencies. We also compete in our mortgage insurance business with structured transactions in the capital markets and with other financial instruments designed to manage credit risk, such as credit default swaps and credit linked notes, with lenders who forego mortgage insurance, or self-insure, on loans held in their portfolios, and with lenders that provide mortgage reinsurance through captive

19

mortgage reinsurance programs. In Canada and some European countries, our mortgage insurance business competes directly with government entities, which provide comparable mortgage insurance. Government entities with which we compete typically do not have the same capital requirements and do not have the same profit objectives as we do. Although private companies, such as our company, establish pricing terms for their products to achieve targeted returns, these government entities may offer products on terms designed to accomplish social or political objectives or reflect other non-economic goals.

In many of our product lines, we face competition from competitors that have greater market share or breadth of distribution, offer a broader range of products, services or features, assume a greater level of risk, have lower profitability expectations or have higher financial strength ratings than we do. Many competitors offer similar products and use similar distribution channels. The substantial expansion of banks' and insurance companies' distribution capacities and expansion of product features in recent years have intensified pressure on margins and production levels and have increased the level of competition in many of our business lines.

We may be unable to attract and retain independent sales intermediaries and dedicated sales specialists.

We distribute our products through financial intermediaries, independent producers and dedicated sales specialists. We compete with other financial institutions to attract and retain commercial relationships in each of these channels, and our success in competing for sales through these sales intermediaries depends upon factors such as the amount of sales commissions and fees we pay, the breadth of our product offerings, the strength of our brand, our perceived stability and our financial strength ratings, the marketing and services we provide to them and the strength of the relationships we maintain with individuals at those firms. From time to time, due to competitive forces, we have experienced unusually high attrition in particular sales channels for specific products. Our inability to continue to recruit productive independent sales intermediaries and dedicated sales specialists, or our inability to retain strong relationships with the individual agents at our independent sales intermediaries, could have an adverse effect on our financial condition and results of operations.

If the counterparties to our reinsurance arrangements or to the derivative instruments we use to hedge our business risks default, we may be exposed to risks we had sought to mitigate, which could adversely affect our financial condition and results of operations.

We use reinsurance and derivative instruments to mitigate our risks in various circumstances. Reinsurance does not relieve us of our direct liability to our policyholders, even when the reinsurer is liable to us. Accordingly, we bear credit risk with respect to our reinsurers. We cannot assure you that our reinsurers will pay the reinsurance recoverable owed to us now or in the future or that they will pay these recoverables on a timely basis. A reinsurer's insolvency or inability or unwillingness to make payments under the terms of its reinsurance agreement with us could have an adverse effect on our financial condition and results of operations.

Prior to the completion of this offering, we will cede to UFLIC, effective as of January 1, 2004, policy obligations under our structured settlement contracts, which had reserves of $12.0 billion, and our variable annuity contracts, which had general account reserves of $2.8 billion and separate account reserves of $7.9 billion, in each case as of December 31, 2003. These contracts represent substantially all of our contracts that were in force as of December 31, 2003 for these products. In addition, effective as of January 1, 2004, we will cede to UFLIC policy obligations under a block of long-term care insurance policies that we reinsured from Travelers, which had reserves of $1.5 billion as of December 31, 2003. UFLIC has agreed to establish trust accounts for our benefit to secure its obligations under the reinsurance arrangements, and General Electric Capital Corporation, an indirect subsidiary of GE, or GE Capital, has agreed to maintain UFLIC's risk-based capital above a specified minimum level. If UFLIC becomes insolvent notwithstanding this agreement, and the amounts in the trust accounts are insufficient to pay UFLIC's obligations to us, our financial condition and results of

20

operations could be materially adversely affected. See "Arrangements between GE and our Company—Reinsurance Transactions."

In addition, we use derivative instruments to hedge various business risks. We enter into a variety of derivative instruments, including options, forwards, interest rate and currency swaps and options to enter into interest rate and currency swaps with a number of counterparties. If our counterparties fail to honor their obligations under the derivative instruments, our hedges of the related risk will be ineffective. That failure could have an adverse effect on our financial condition and results of operations.

Fluctuations in foreign currency exchange rates and international securities markets could negatively affect our profitability.

Our international operations generate revenues denominated in local currencies. For the three months ended March 31, 2004 and 2003, and the years ended December 31, 2003, 2002 and 2001, respectively, 20%, 16%, 18%, 14% and 14% of our revenues, and 32%, 23%, 26%, 12% and 11% of our net earnings from continuing operations were generated by our international operations. We generally invest cash generated by our international operations in securities denominated in local currencies. As of each of March 31, 2004 and December 31, 2003 and 2002, approximately 5% of our invested assets were held by our international operations and were invested primarily in non-U.S.-denominated securities. Although investing in securities denominated in local currencies limits the effect of currency exchange rate fluctuation on local operating results, we remain exposed to the impact of fluctuations in exchange rates as we translate the operating results of our foreign operations into our combined financial statements. We currently do not hedge this exposure, and as a result, period-to-period comparability of our results of operations is affected by fluctuations in exchange rates. For example, our net earnings for the three months ended March 31, 2004 and the year ended December 31, 2003, included approximately $12 million and $25 million, respectively, due to the favorable impact of changes in foreign exchange rates. In addition, because we derive a significant portion of our earnings from non-U.S.-denominated revenue, our results of operations could be adversely affected to the extent the dollar value of non-U.S.-denominated revenue is reduced due to a strengthening U.S. dollar.

In addition, our investments in non-U.S.-denominated securities are subject to fluctuations in non-U.S. securities and currency markets, and those markets can be volatile. Non-U.S. currency fluctuations also affect the value of any dividends paid by our non-U.S. subsidiaries to their parent companies in the U.S. For additional information regarding the sensitivity of our net earnings to foreign currency exchange rate fluctuations, see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Quantitative and Qualitative Disclosures About Market Risk—Sensitivity analysis."

Our insurance businesses are heavily regulated, and changes in regulation may reduce our profitability and limit our growth.

Our insurance operations are subject to a wide variety of laws and regulations. State insurance laws regulate most aspects of our U.S. insurance businesses, and our insurance subsidiaries are regulated by the insurance departments of the states in which they are domiciled and licensed. Our non-U.S. insurance operations are regulated principally by insurance regulatory authorities in the jurisdictions in which they are domiciled.

State laws in the U.S. grant insurance regulatory authorities broad administrative powers with respect to, among other things:

21

State insurance regulators and the National Association of Insurance Commissioners, or NAIC, regularly re-examine existing laws and regulations applicable to insurance companies and their products. Changes in these laws and regulations are often made for the benefit of the consumer at the expense of the insurer and thus could have an adverse effect on our financial condition and results of operations.

Our mortgage insurance business is subject to additional laws and regulations. For a discussion of the risks associated with those laws and regulations, see "—Risks Relating to Our Mortgage Insurance Business—Changes in regulations that affect the mortgage insurance business could affect our operations significantly and could reduce the demand for mortgage insurance."

Currently, the U.S. federal government does not regulate directly the business of insurance. However, federal legislation and administrative policies in several areas can significantly and adversely affect insurance companies. These areas include financial services regulation, securities regulation, pension regulation, privacy, tort reform legislation and taxation. In addition, legislation has been introduced in the U.S. Senate, which, if enacted, would establish comprehensive and exclusive federal regulation over all "interstate insurers." This legislation would repeal the McCarran-Ferguson antitrust exemption for the business of insurance. It would also establish a Federal Insurance Regulatory Commission within the Department of Commerce that would have exclusive regulatory jurisdiction over life and property and casualty insurers that do business in more than one U.S. jurisdiction. The legislation would establish comprehensive federal regulatory oversight over such insurers, including licensing, solvency supervision, accounting and auditing practices, form and rate approval, and market conduct examination. In particular, the legislation would provide for price regulation of life insurance products, which is not now a feature of state regulation of life insurance and could affect the profitability of this business. The legislation also would establish a National Insurance Guaranty Fund which may be empowered to collect pre-funded assessments that are different from, and potentially greater than, current state guaranty fund assessment levels.

The Federal Trade Commission and the Federal Communications Commission have promulgated regulations governing telemarketing practices, including the implementation of a national Do-Not-Call Registry. These regulations require telemarketers under the jurisdiction of either agency to consult the Do-Not-Call Registry periodically and to remove from telemarketing lists any telephone numbers on that registry before making telemarketing calls. Under the McCarran-Ferguson Act, insurers are not subject to these regulations to the extent that their telemarketing activities constitute the "business of insurance" regulated by state law. Nevertheless, we believe it is not clear whether either agency will attempt to assert jurisdiction over any insurer that engages in telemarketing activities. We believe these regulations already have had an adverse effect, and may have a further adverse effect, on our sales of insurance products, such as long-term care insurance, that we market partly through telemarketing calls.

Our international operations are subject to regulation in the relevant jurisdictions in which they operate, which in many ways is similar to that of the state regulation outlined above. See "Regulation—International Regulation."

22

Many of our customers and independent sales intermediaries also operate in regulated environments. Changes in the regulations that affect their operations also may affect our business relationships with them and their ability to purchase or to distribute our products. Accordingly, these changes could have an adverse effect on our financial condition and results of operation.

Compliance with applicable laws and regulations is time consuming and personnel-intensive, and changes in these laws and regulations may increase materially our direct and indirect compliance and other expenses of doing business, thus having an adverse effect on our financial condition and results of operations. For a further discussion of the regulatory framework in which we operate, see "Regulation."

Legal and regulatory investigations and actions are common in the insurance business and may result in financial losses and harm our reputation.

We face significant risks of litigation and regulatory investigations and actions in connection with our activities as an insurer, financial services provider, employer, investment adviser, securities issuer, investor and taxpayer. These lawsuits and regulatory actions may be difficult to assess or quantify and may seek recovery of very large or indeterminate amounts, including punitive and treble damages, which may remain unknown for substantial periods of time. A substantial legal liability or a significant regulatory action against us could have an adverse effect on our financial condition and results of operations. Moreover, even if we ultimately prevail in the litigation, regulatory action or investigation, we could suffer significant reputational harm, which could have an adverse effect on our business.

Life insurance companies historically have been subject to substantial litigation resulting from policy disputes and other matters. Most recently, they have faced extensive claims, including class-action lawsuits, alleging improper life insurance sales practices. Judgments or negotiated settlements of such claims have had an adverse impact on the financial condition and results of operations of other insurance companies. We recently agreed to settle one such case and have established what we believe are adequate reserves to bring the matter to a conclusion. Substantial legal liability in any of these or future legal or regulatory actions could have an adverse financial effect or cause significant reputational harm. For further details regarding the litigation in which we are involved, see "Business—Legal Proceedings."

We have significant operations in India that could be adversely affected by changes in the political or economic stability of India or government policies in India, the U.S. or Europe.

Through an arrangement with an affiliate of GE, we have a substantial team of professionals in India who provide a variety of services to our insurance operations, including customer service, transaction processing, and functional support including finance, investment research, actuarial, risk and marketing. See "Arrangements Between GE and Our Company—Relationship with GE—Arrangements Regarding Our Operations in India." The development of our operations center in India has been facilitated partly by the liberalization policies pursued by the Indian government over the past decade. The current government of India, formed in October 1999, has announced policies and taken initiatives that support the continued economic liberalization policies that have been pursued by previous governments. However, we cannot assure you that these liberalization policies will continue in the future. The rate of economic liberalization could change, and specific laws and policies affecting our business could change as well. A significant change in India's economic liberalization and deregulation policies could adversely affect business and economic conditions in India generally and our business in particular.

The political climate in the U.S. also could change so that it would not be practical for us to use international operations centers, such as call centers. This could adversely affect our ability to maintain or create low-cost operations outside the U.S. For example, a bill recently introduced in the U.S. Senate, entitled "The Call Center Consumer's Right To Know Act," would, if enacted, require employees of call centers used by a U.S. company to disclose their physical location at the beginning of each telephone call. An identical bill recently was introduced in the U.S. House of Representatives.

23

Similar legislation also is pending in several states in which we operate. We believe the intent of this legislation is to alert consumers to the use of call centers that are located outside the U.S. If enacted, this legislation could result in consumer pressure to curtail our use of low-cost operations outside the U.S., which could reduce the cost benefits we currently realize from using them.

Similarly, the political or regulatory climate in Europe could change in ways which would inhibit our ability to use international operations centers. For example, changes in European privacy regulations, or more stringent interpretation or enforcement of these regulations, could require us to curtail our use of low-cost operations in India to service our European businesses, which could reduce the cost benefits we currently realize from using these operations.

The continued threat of terrorism, the occurrence of terrorist acts and ongoing military actions could adversely affect our financial condition and results of operations.

The continued threat of terrorism and ongoing military actions, as well as heightened security measures in response to these threats and actions, may cause significant volatility in global financial markets, disruptions to commerce and reduced economic activity. These consequences could have an adverse effect on the value of the assets in our investment portfolio. We cannot predict whether, and the extent to which, companies in which we maintain investments may suffer losses as a result of financial, commercial or economic disruptions, or how any such disruptions might affect the ability of those companies to pay interest or principal on their securities. The continued threat of terrorism also could result in increased reinsurance prices and potentially cause us to retain more risk than we otherwise would retain if we were able to obtain reinsurance at lower prices. In addition, the occurrence of terrorist actions could result in higher claims under our insurance policies than we had anticipated. For example, we incurred approximately $25 million in losses related to the terrorist events of September 11, 2001.

Risks Relating to Our Protection and Retirement Income and Investments Segments

We may face losses if morbidity rates, mortality rates or unemployment rates differ significantly from our pricing expectations.